A股入摩:对国内市场有什么影响?

编者按:本文来自微信公众号“洪灝的中国市场策略”(ID:honghaochinastrategy)。原题目《A股入摩:历史性时刻后的思考》

概要 - A股纳入MSCI的起始权重虽小,但是仍然比预期稍大。中国在重新监管股票停牌、扩大互联互通机制、放宽新产品的预审权以及国际社会的支持帮助了A股这次成功入摩。因此,市场的最初的反应应该是正面的,尤其是对于入摩最受惠的大盘蓝筹股。

Summary - The MSCI inclusion is small, but slightly higher than expected. China’s efforts on re-regulating stock trading suspension, as well as the expansion of the Connect Scheme, and the relaxation of new product preapproval and the support of the international investment community have worked. As such, initial market reaction should be positive, especially towards the larger caps.

然而未来挑战仍存。A股不同的交易环境往往难以理喻,国际基金经理将难以适应。入摩后, A股的估值很可能将逐渐降至国际水平。与此同时,全球贸易领先指标已见顶,预示全球增长将放缓。无论入摩与否,经济增长放缓的环境里应配置大盘蓝筹股。本文里,我们避免解释那些众所周知的情况,而提出了一些市场共识可能会忽略的问题。

However, A-shares can be inscrutable, with a different trading environment that international fund managers will find it hard to adapt to. Over time, inclusion will likely lower A-shares’ valuation to the international level. The global trade leading indicator has peaked, portending moderating growth ahead. While the inclusion bodes well for large-cap blue chips, slowing growth suggests allocations towards these stocks, with or without the inclusion. In this short note, we avoid stating the obvious, but raise some questions that consensus may have missed instead.

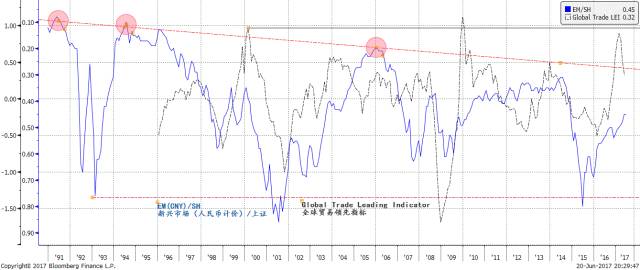

焦点图表一:全球贸易领先指标已见顶。新兴市场虽跑赢上证,但是新兴市场里最容易的钱已经赚到了。

Focus Chart 1: Global trade growth has peaked. EM outperforms Shanghai, but the easiest gain is behind us.

中国进入MSCI全球指数是一个历史时刻。经过三年的申请,中国市场国际化的万里长征似乎能够看到终点。然而,未来的挑战仍存:

China’s entry into the MSCI global indices is a historic milestone. The goal of China’s long march towards global markets is now finally in sight, after three years of bidding. But challenges remain:

1)全球贸易领先指标见顶,预示着增长将放缓(焦点图表一)。我们的其他领先指标模型也勾勒出增长放缓的前景(《2017年下半年展望:要命的不漂亮,漂亮的不要命》,20170609)。中国有着一个庞大的国内市场,消费的增长现在已经占全国经济增长的一半。全球贸易的放缓对其他新兴市场可能影响更大。 因此,新兴市场相对于上海的相对回报在未来数月将会减弱。但由于只是小范围纳入,中国对MSCI新兴市场指数回报的贡献有限。

1) The leading indicator for global trade growth has peaked, hinting at moderating growth ahead (Focus Chart 1). Our other leading indicator models are also pointing to slower growth (“2H17 Outlook: An Idiot’s Guide to China’s Nifty-Fifty Run", 20170609). Presumably, as China has a substantial domestic market, and consumption now contributes half of the country’s economic growth, slowing global trade will likely affect other emerging markets more. Thus, EM’s performance relative to Shanghai will wane in the coming months. But small inclusion limits the contribution of Shanghai to the MSCI EM index return.

2)小范围纳入意味着最初纳入的指数权重减少到0.7%,相当于增加资金流入约100亿美元。在一个市值约为8万亿美元,每天交易约500亿美元的市场里,这样的新增资金规模无疑是九牛一毛。中国市场有自己的深度,并不真的像很多人所想的“需要外援”。纳入后带来的增量资金太小,对交易情绪的提振可能更大于增量资金的流入。此外,为了避免在一个不了解情况的市场里投资,追踪MSCI指数的主动型资金基金经理在构建他们的投资组合时可以选择不包括A股,因为其指数权重太小,不太可能影响基金表现。

2) The scaled-down inclusion means less index weight of 0.7% initially, equivalent to incremental fund inflow of around USD 10 billion in a market that is ~USD 8 trillion in size, and trades ~USD 50 billion or more a day. The Chinese market has depth, and does not really need “foreign rescue” as many suggest. The lift on sentiment in the near term will be much more significant than the incremental fund flow initially. Further, to avoid an inscrutable market, active funds that tend to track MSCI indices can opt not to include A-shares in their portfolios, as its small index weight is unlikely to sway performance.

3)与国际市场相比,中国市场估值偏高。例如,长期以来被视为中国近似市场的香港,虽然香港上市公司有70%以上的盈利来自大陆,但是H股相对于A股仍有20%的折让。随着纳入权重的进一步推进,中国市场的全球化很有可能将A股估值降至全球水平。

3) The Chinese market has higher valuation compared with international markets. For instance, Hong Kong, long regarded as a China proxy with more than 70% of listed companies’ earnings from the mainland, is still seeing 20% discount of its H-shares relative to A-shares. The global integration of the Chinese market will likely lower A-shares’ valuation to the global level.

4)现在暂时难以估计究竟会是A股国际化,还是恰恰相反。 最近三地互联互通计划启动以来的经验似乎表明,A股的交易员正在采用有时并不完全合规的交易策略,在香港进行交易,并引发了一些股票剧烈波动。国际基金经理可能不得不适应A股的交易环境,就像古时候蒙古人被汉族同化一样。

4) It is difficult to gauge whether A-shares will adapt to international best practices, or the other way around. Recent experience since the launch of the Connect Program seems to suggest that traders from A-shares are applying their trading strategies, at times not entirely legitimate, to trading in Hong Kong, triggering violent swings in some stocks. International fund managers may have to acclimatize to A-shares’ trading environment, much like how the Mongol warriors were “tamed” by the ancient Han.

洪灝,CFA

2017-06-21